Around 97 percent of outstanding first-lien, closed-end residential mortgages in the United States, and 98.5 percent of those the Enterprises acquired, have home equity above 10 percent. Only 0.2 percent of these mortgages have negative equity, the lowest level in the past 10 years.

Introduction

On June 30, 2023, the Federal Housing Finance Agency (FHFA) released the quarterly National Mortgage Database (NMDB®) Aggregate Statistics,1 which cover outstanding first-lien, closed-end residential mortgages from the first quarter of 2013 through the same period of 2023. In this blog, we use a subset of data to explore home equity at the national level.

Home equity refers to the market value of homeowners’ unencumbered interest in their real property, or the difference between the home's current market value and the outstanding balance of all liens on the property. Home equity is an important asset that homeowners can potentially tap into for purposes such as financing home improvements, paying off high-interest debts, funding education expenses, or investing in other properties. Building equity in a home typically occurs over time through repaying the mortgage principal. Homeowners can also build equity through an increase in the home's value either through home improvements or price appreciation.

One of several ways to calculate home equity is to subtract the outstanding mortgage balance from the home's current market value. For example, if a property is currently valued at $300,000, and the homeowner owes $200,000 on the mortgage, the home equity would be $100,000, or 33.3 percent of the property value. One of the fields available in the NMDB Aggregate Statistics is the current mark-to-market (MTM) loan-to-value (LTV) ratio, which reflects what a homeowner owes on their first-lien mortgage divided by the property value of the home. In our example above, the MTM LTV ratio would equal $200,000 divided by $300,000, or 66.7 percent. Thus, we can calculate home equity as 1 – MTM LTV ratio = 1 – 66.7 percent = 33.3 percent.2

We calculate four categories of homeowner equity using data available in the NMDB Aggregate Statistics.3 These four categories include home equity:

- Greater than or equal to 30 percent,

- From 10 to 29.9 percent,

- From 0 to 9.9 percent, and

- Less than 0 percent (negative) home equity.

Additionally, we present analyses for all market segments, combined and separately, for the following three market segments:

- Enterprise Acquisitions - mortgages acquired by either Fannie Mae or Freddie Mac,

- Government/Non-Conventional (“Government-backed”) - mortgages insured or guaranteed by the Federal Housing Administration (FHA), U.S. Department of Veterans Affairs (VA), or Rural Housing Service (RHS) in the U.S. Department of Agriculture (USDA), and

- Other Conventional - other conforming and jumbo mortgages.

Table 1 presents the number and outstanding balance of active mortgages as of the end of Q1 2023 for each market segment. There were slightly more than 50 million first lien, closed-end mortgages in the United States, with $11.27 trillion in current balance (or outstanding principal balance). By loan count, Enterprise acquisitions accounted for nearly 59 percent, followed by Government-backed with 22 percent, and Other Conventional with 19 percent. The percentages in terms of outstanding principal balance are 56 percent, 19 percent, and 25 percent, respectively. The Other Conventional market contains jumbo mortgages, which largely drives the difference between its share in terms of count versus its share in terms of current balance.

Table 1: Number and Balance of Active Residential Mortgages as of Q1 2023

| Number of loans (Thousand) | Current Balance ($Trillions) | |

|---|---|---|

| Enterprise Acquisitions | 29,570 | 6.32 |

| Government/Non-Conventional | 10,923 | 2.16 |

| Other Conventional | 9,738 | 2.79 |

| Total Market | 50,231 | 11.27 |

Note: The NMDB is a 5 percent sample and not a census of all mortgages.

Home Equity for the Total Market

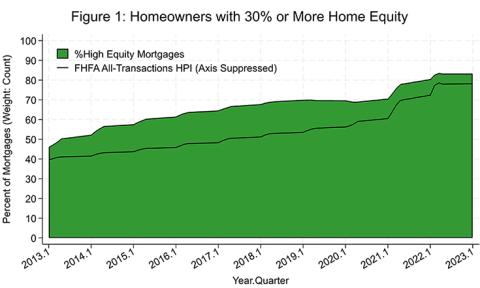

Nationally, as depicted in Figure 1, the percentage of mortgages with equity of more than or equal to 30 percent (high equity) has increased steadily from 46.1 percent in Q1 2013 to a 10-year high of 83.3 percent by Q1 2023. However, the percentage of high equity mortgages has been relatively constant over the past year.

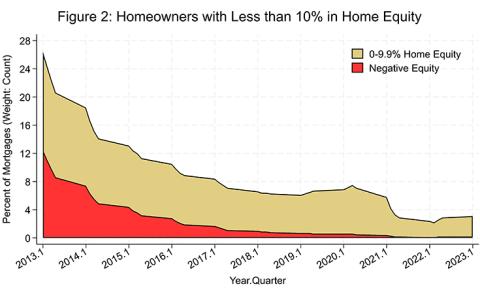

This trend is largely consistent with house price appreciation through this period. Most homeowners who purchased or refinanced their properties prior to Q2 2022 have seen large home price appreciation, and consequently, large increases in home equity, causing only 0.2 percent of mortgages to have negative equity, the lowest value since 2013. Figure 2 presents the percentage of mortgages in the bottom two homeowner equity buckets.

While house price appreciation has helped increase home equity, if house prices were to decline 10 percent,4 homeowners with current equity of 10 percent or less (low equity) would go “underwater” or have negative equity, owing their lender more than the property’s worth. Nationally, the percentage of low equity mortgages has started to increase, from 2.2 percent in Q2 2022 to 3.1 percent in Q1 2023. This implies that a nationwide house price decline of 10 percent would result in over 1.5 million homeowners with negative equity. The number of low equity mortgages, however, remains historically low.

Homeowner Equity by Market Segments

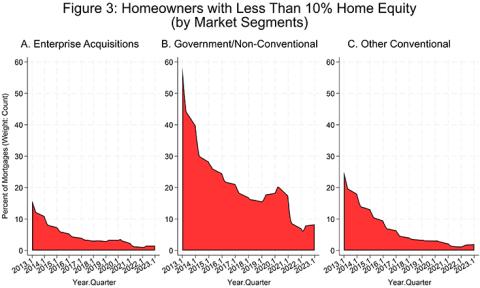

The level of home equity varies significantly by market segment. Figure 3 shows that the percentage of low equity mortgages has generally been declining over time for each of the three market segments. However, the percentage of low equity mortgages has been much higher in the Government-backed segment (currently 8.3 percent) compared to 1.5 percent for Enterprise acquisitions and 2.0 percent for Other Conventional, respectively, as of Q1 2023.

These results are not surprising given that mortgages in the Government-backed market segment are popular among homebuyers with limited downpayment funds. FHA mortgages typically require a minimum down payment of 3.5 percent of the purchase price, and many VA loans do not require any down payments. A down payment indicates the initial level of home equity, with a low-down payment associated with low home equity for new mortgages. As the mortgage matures, the equity changes based on the homeowner’s payments towards principal, home improvements, and house price appreciation.

Summary

The NMDB Aggregate Statistics data suggest that the percentage of mortgages with low equity is at a low level (about 3 percent as of Q1 2023), with the figure significantly lower in the Enterprises Acquisition and Other Conventional market segments compared to the Government-backed market segment.

We encourage readers to explore the NMDB Aggregate Statistics on the FHFA website.

1 FHFA and the Consumer Financial Protection Bureau jointly fund and manage the NMDB program.

2 The NMDB includes only first-lien mortgages that are reported to one of the three major credit bureaus. Therefore, the estimates for homeowners’ equity in their homes based on NMDB Aggregate Statistics are likely to be an overestimate since the calculation does not account for second liens and other potential encumbered interests. However, the second liens and other potential encumbered interests account for less than 1 percent of the principal balance securitized by the Enterprises.

3 The published NMDB Aggregate Statistics report data for six categories of MTM LTV ratio, providing additional detail for users interested in creating additional home equity categories.

4 Economists expect the U.S. housing market to cool in 2023 but little consensus exists on the change in house prices. For example, Moody's (Source: Moody’s Data Buffet) is forecasting the quarterly FHFA Purchase-Only HPI to fall to -3.3% (Year-over-Year) in Q3 2024 and be at -2.9% in Q4 2024. Goldman Sachs revised its forecast in June 2023 for house price decline from above 6 percent by year-end to under 3 percent for 2023. The Mortgage Bankers Association (MBA) (Source: Bloomberg) and Fannie Mae forecast HPI to drop by less than one percent by Q1 2024, and MBA expects mild recovery by year-end 2024.

Tagged: FHFA Stats Blog; Home Equity; Aggregate Statistics; Data; Open Data; Source: FHFA

By: Anju Vajja

FHFA Research Officer

Division of Research and Statistics