Financing of multifamily properties by Fannie Mae and Freddie Mac in areas of concentrated poverty, as well as their financing of mixed-income housing in these areas, reached a five-year high in 2022. However, absolute dollar financing of mixed-income housing remains small compared to all other financing in these areas.

Introduction

On September 30, 2023, the Federal Housing Finance Agency (FHFA) released the annual Public Use Databases (PUDB), which contain information about Fannie Mae and Freddie Mac’s (the Enterprises) single-family and multifamily mortgage acquisitions.1 In this blog, we explore the Enterprises’ acquisitions of mortgages backing multifamily housing in areas of concentrated poverty (ACPs).

Areas of Concentrated Poverty

Areas of concentrated poverty (ACPs) are often defined as geographical areas where a high proportion of residents live below the poverty line.2 FHFA defines an ACP as a census tract that the Department of Housing and Urban Development designates either as (a) a Qualified Census Tract, pursuant to 26 U.S.C. 42(5)(B)(ii), or (b) a Racially- or Ethnically-Concentrated Area of Poverty, pursuant to 24 CFR 5.152, during any year an Enterprise’s Duty to Serve Underserved Markets Plan covers or in the year prior to a plan's effective date.3 Starting in 2018, the PUDB Multifamily Census Tract Files include a flag for any geographical area that the FHFA’s Duty to Serve regulation identifies as an ACP. From 2018–2022, the PUDB includes about 7,000 geographical areas flagged as ACPs and about 17,000 not flagged as ACPs (non-ACPs).

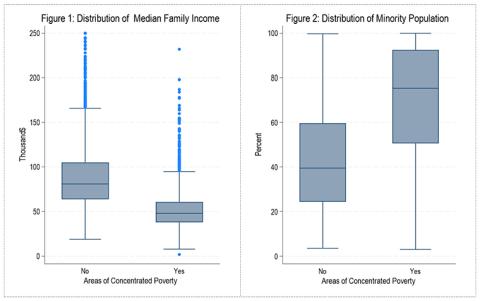

ACPs are less likely to feature high-quality educational, health, and investment opportunities relative to non-ACPs. These census tracts also are more likely to have higher crime rates and lower family wealth and income.4 For ACPs in which the Enterprises provided multifamily financing in 2022, the distribution of the area median income (AMI) was significantly different from the distribution of the AMI for non-ACPs in which the Enterprises provided multifamily financing.5 The 2022 AMI ranged between $26,000 and $95,000 for 90 percent of the ACPs. This range was between $46,000 and $158,000 for non-ACPs (which the horizontal lines at the end of each box chart depict in Figure 1). The real median household income for the United States in 2022 was $74,580, but the median AMI in ACPs was approximately $48,000 and approximately $81,000 in non-ACPs.

In ACPs, the minority share of the population also tends to be higher. Figure 2 presents the distribution of the percentage of minority population for ACPs and non-ACPs.6 While the range of the percentages of minority population was similar for ACPs and non-ACPs, the distribution was noticeably different (see box chart in Figure 2). For the majority of ACPs, the minority population was higher than 75 percent of the total population, but the minority population was less than 40 percent in the majority of non-ACPs.

Multifamily Properties in ACPs

Investment and development in ACPs have been part of the Enterprises’ Duty to Serve Underserved Markets Plans since 2018.7 Table 1 presents information on the financing of multifamily properties by the Enterprises in ACPs over the past five years. In 2022, the Enterprises provided $36.7 billion in multifamily housing financing support in ACPs for approximately 3,700 properties, which was over a quarter of their total multifamily housing financing.8 The table demonstrates that the Enterprises’ footprint in ACPs increased substantially in 2022 compared to 2018–2021, both in the number of multifamily properties in ACPs and in the share of financing in ACPs as compared to their total multifamily financing.9

Table 1: Enterprises’ Multifamily Financing in ACPs

| 2018 | 2019 | 2020 | 2021 | 2022 | |

|---|---|---|---|---|---|

| Number of properties in ACPs (thousands) | 3.2 | 3.1 | 3.5 | 3.0 | 3.7 |

| Financing in ACPs ($ billions) | 30.6 | 30.9 | 35.0 | 29.9 | 36.7 |

| Financing in ACPs as % of total financing | 23.1 | 22.3 | 23.9 | 22.9 | 27.4 |

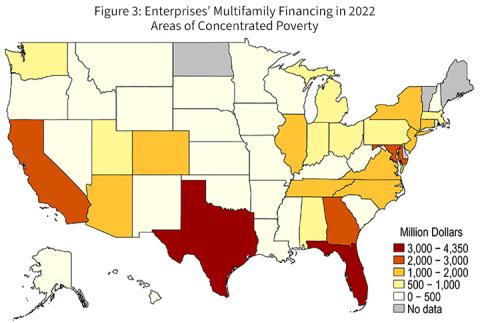

Figure 3 presents the distribution of the Enterprises’ $36.7 billion in financing across the states and the District of Columbia. While the Enterprises financed multifamily properties in ACPs in nearly all states, seven states (Arizona, California, Georgia, Florida, Maryland, New York, and Texas) accounted for over 50 percent of these funds. It is important to note that Alabama, Arkansas, Kentucky, Louisiana, Mississippi, New Mexico, Oklahoma, and West Virginia have poverty rates of 15 percent or higher and have many census tracts with persistent high poverty rates but have relatively low multifamily financing in designated ACPs.10 Multifamily properties, in general, tend to be less prevalent in less urbanized states.

Figure 4 presents the percentage of Enterprise financing that has supported mixed-income multifamily housing over the past five years.11 In 2022, nearly 45 percent of Enterprise-financed mixed-income multifamily housing was in ACPs, though the $2.3 billion was less than 7 percent of their total multifamily housing financing in ACPs. This is an area where the Enterprises potentially could increase their efforts, as mixed-income multifamily housing promotes the socioeconomic development of neighborhoods and improves the economic viability of multifamily housing.12 Freddie Mac research indicates that mixed-income multifamily housing in high-poverty neighborhoods is a potential way to reduce concentrated levels of poverty.13 That said, the Enterprises’ financing of mixed-income housing in ACPs has increased from 5 percent in 2018 to 7 percent in 2022, the highest level since FHFA started collecting this data.

Summary

PUDB multifamily data suggests that the Enterprises financed a five-year high in ACPs in 2022, both in absolute dollar financing and relative to financing for all multifamily properties. The Enterprises also increased their financing of mixed-income housing in ACPs, though this remains a small portion of their aggregate financing in ACPs.

We encourage readers to explore the PUDB datasets on the FHFA website.

1 https://www.fhfa.gov/data/public-use-database-fannie-mae-and-freddie-mac.

2 According to the Annie E. Casey Foundation, “[a]reas of concentrated poverty are defined as census tracts where the overall poverty rate checks in at 30 percent or more.” (Concentrated Poverty - The Annie E. Casey Foundation (https://www.aecf.org/topics/concentrated-poverty)). The official U.S. 2022 poverty rate was 11.5 percent. (Poverty in the United States: 2022 (census.gov))

3 https://www.fhfa.gov/Areas_of_Concentrated_Poverty_README_2022.pdf

4 https://aspe.hhs.gov/reports/overview-community-characteristics-areas-concentrated-poverty

5 We base the 2022 median family income for the census tract on 2020 Census geography and the most recent American Community Survey (ACS) five-year estimates available on January 1, 2022.

6 The PUDB Multifamily Census Tract File contains a field capturing the census tract’s population classified as belonging to a minority group, based on the 2020 Census, with the definition of “minority” that 12 CFR 1282.1 defines.

7 FHFA issued a final rule to implement the statutory requirements, effective January 30, 2017 (81 FR 96242 (December 29, 2016)). The Agency required each Enterprise to submit an Underserved Markets Plan covering a three-year period that describes the activities and objectives it will undertake in each underserved market to meet its duty to serve. The Enterprises’ first plans covered January 2018 to December 2021, as the plans were extended during the pandemic. (Duty to Serve Program | Federal Housing Finance Agency (fhfa.gov)).

8 The multifamily data does not contain about $9 billion of properties (six percent of total Enterprise mortgage acquisitions) that are ineligible for Enterprise Housing Goals credit. Also, to conform with Consumer Financial Protection Bureau (CFPB) Privacy Guidance, FHFA reports acquisition balance of debt financing and property values as the midpoint for the $10,000 interval into which the reported value falls.

9 We can partially explain these higher numbers with the incorporation of 2020 Census in the 2022 PUDB files.

10 Poverty in States and Metropolitan Areas: 2022 (census.gov).

11 We define mixed-income housing as properties in which no more than 80 percent, but at least 20 percent, of the units are income-restricted pursuant to federal, state, or local affordable housing programs. For the purpose of Duty to Serve, a mixed-income property is one that satisfies both of the following two conditions: (i) at least 20 percent of the units must be affordable to households making 50 percent of the AMI or at least 40 percent of the units must be affordable to households making 60 percent of the AMI; and (ii) at least 20 percent of the units must be unaffordable to households making less than 80 percent of the AMI.

12 www.huduser.gov/portal/periodicals/em/spring13/highlight1.html

13 https://freddiemac.gcs-web.com/news-releases/news-release-details/freddie-mac-multifamily-white-paper-examines-mixed-income

Tagged: FHFA Stats Blog; Source: FHFA; Public Use Database; Enterprises; Areas of Concentrated Poverty (ACPs)

By: Anju Vajja

FHFA Research Officer

Division of Research and Statistics