In the aftermath of the destruction spanning North Carolina to Florida following Hurricanes Helene and Milton in late September and early October, many residents of this region face a long road to recovery. The Federal Housing Finance Agency (FHFA) today published a dashboard with data on single-family mortgages backed by Fannie Mae and Freddie Mac (the Enterprises) in counties affected by these storms. Our goal is to provide valuable data for decision makers as they consider how best to support victims of these storms and reduce the impact of future natural disasters.

FHFA analysis of Enterprise data suggests that at least 2.5 million single-family home loans backed by the Enterprises are in counties deemed eligible for Individual Assistance grants from the Federal Emergency Management Agency (FEMA) after Hurricanes Helene and Milton. For these loans, the average homeowner still owes roughly $200,000, and the total unpaid principal balance (UPB) across both Enterprises is over $500 billion (even though only a small portion of that amount might result in losses).

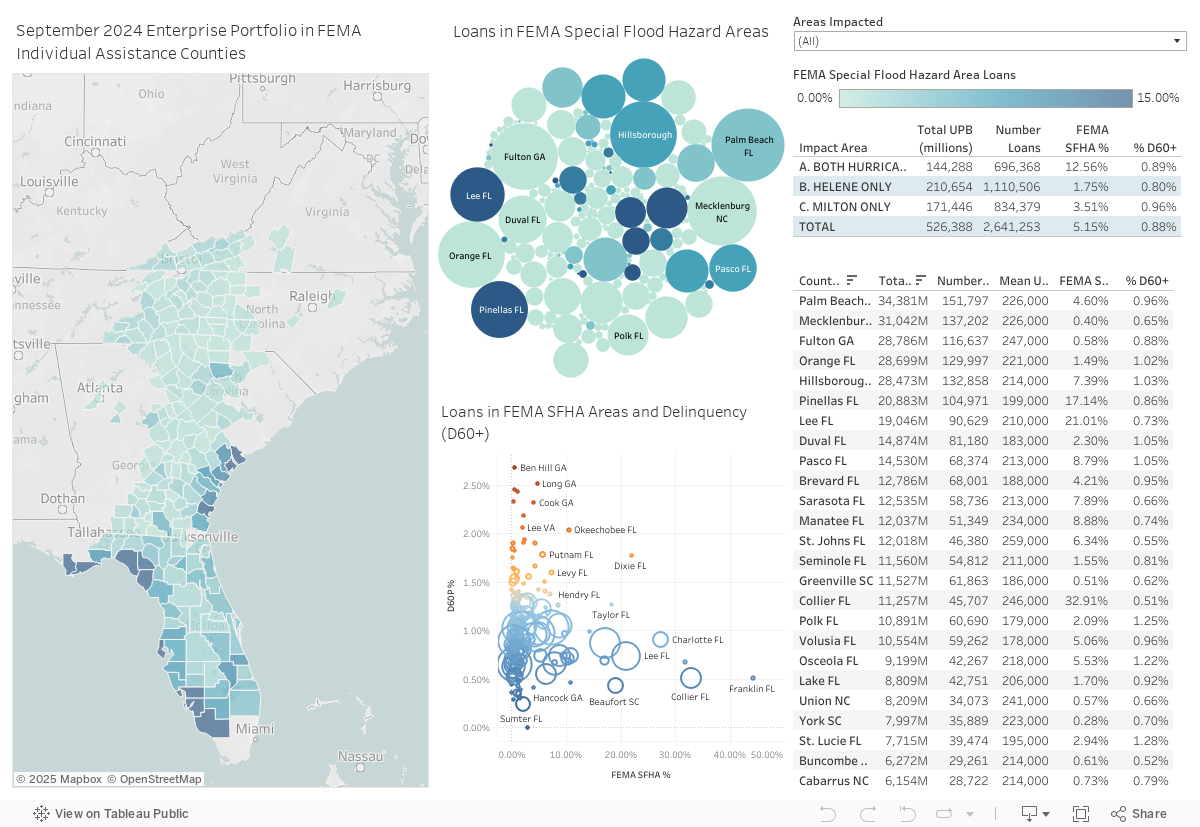

Table 1: Possible Enterprise Exposure for Hurricanes Helene and Milton[1]

| All Portfolio Loans in Disaster Areas | Number of Loans | Total UPB (Millions) | Mean UPB | Percent in FEMA SFHA[2] | Percent D60+ |

|---|---|---|---|---|---|

| A. BOTH HURRICANES | 696,368 | 144,288 | 207,201 | 12.56% | 0.89% |

| B. HELENE ONLY | 1,110,506 | 210,654 | 189,692 | 1.75% | 0.80% |

| C. MILTON ONLY | 834,379 | 171,446 | 205,477 | 3.51% | 0.96% |

| TOTAL | 2,641,253 | 526,388 | 199,295 | 5.15% | 0.88% |

The above dashboard also highlights important data on flood insurance requirements and delinquency rates in areas affected by these natural disasters.[3]

- Few Mortgages in Counties Hit by Hurricanes Likely had Flood Insurance: Fannie Mae and Freddie Mac require that properties in “special flood hazard areas” (SFHAs) carry flood insurance to receive their financing. However, we estimate that only 5.2 percent of homes with Enterprise-backed loans in counties hit by the recent hurricanes were in SFHAs at origination and were required to carry flood insurance (although others may have purchased coverage voluntarily). As typical property insurance does not cover flood damage, these loans may be at increased risk of delinquency if homeowners struggle to make monthly mortgage payments or cover the cost of repairs after the storms.

- Delinquency Rates in Affected Areas were Low Prior to Hurricanes: Both Enterprises have programs that provide consumers mortgage relief for up to a year after a disaster event without any late fees or penalties. As of September 2024, the share of loans in affected areas 60 days or more delinquent (including those in forbearance) sat below one percent. However, initial data shows that the share of loans in relief programs due to natural disasters rose in October, and FHFA research finds that delinquency rates increase after hurricanes – and do so disproportionately for minority and low-income borrowers. FHFA will continue monitoring affected counties for geographic or demographic differences in delinquency rates and relief enrollment.

FHFA is part of the community of federal agencies taking steps to address the growing risk of natural disasters in the United States. We know that existing wealth and income disparities limit underserved communities’ ability to recover from natural disasters. Analysts and decision makers can use this information and other natural disaster risk data to consider how to reduce the impact of future natural disasters, especially in lower-income communities.

[1] Enterprise active single family portfolio loans, excluding government loans and loans with missing UPB.

[2] SFHA status estimated at time of origination based on appraisal records for single family mortgages funded by Fannie Mae and Freddie Mac.

[3] The estimates represent count, sum, mean, and proportion of active portfolio loans as of September 2024 servicing cycle. FHFA is not aware of significant errors in the underlying data used to create statistics in the above dashboard.

[4] Readers may contact PublicInterest@fhfa.gov with any feedback or other information relevant to this blog.

By: Jonathan Liles

Principal Statistician

Office of Policy, Data, and Oversight

Division of Public Interest Examinations

By: Margaret Seikel

Senior Policy Analyst

Office of Policy, Data, and Oversight

Division of Public Interest Examinations